The most memorable institution of 2019

The bull case for SoftBank's Vision Fund

2018 was widely hailed as the year of the scooter. So what/who was 2019 memorable for in the tech world? There are many obvious candidates. Let’s consider a few. Elon Musk and his tweets. Uber’s IPO. WeWork’s lack thereof. Twitter/Facebook’s opposing stances re political advertising. Away’s CEO’s untimely departure. And so on. But the thing that most sticks out to me is the amount of pages of press dedicated to SoftBank’s Vision Fund (SVF). If significance is measured by % of mindshare, SoftBank and SoftBank startups dominated the tech news cycle for most of the year. For that alone, 2019 was the year of SVF and Masayoshi Son.

I have previously written about Vision Fund. And I routinely take underhand jibes at it in my posts. And frankly, they make it quite easy. But today, I’m going to do something different: I will make the bull case for SVF’s existence. Not satisfied with being labelled a contrarian, I now aim to be a contra-contrarian. I will henceforth argue both sides of an argument in public so that I may conveniently cherry-pick and throw my weight behind the winning side in the future.

Anyways, let’s start with the rules of this game. Let’s put ourselves in the shoes of our protagonists. You are wealthy, powerful and well-connected. But people tell you that you got lucky and there’s this sense that you haven’t really made anything of your own. So you decide to start a mega-fund and ask your rich pals (who suffer from the same insecurities) to chip in. What might the guiding vision of this large investment vehicle be? It’s a lot of fancy words about innovation and technology. But ultimately, it is really about making a difference. It is about getting noticed. Most crucially, it is about having impact. Now impact isn’t just earning a >3x MoM, >8% IRR for your LP investors. Sure, it’s a nice-to-have and often a pre-requisite for GPs to earn their carry. But let’s expand our imaginations a bit here. Here is what Fred Wilson had to say on impact in a post published a few hours ago:

The last two lines are key. Let’s re-read them so that we remember them as we evaluate SVF’s investments.

Even if Tesla fails as a company (which I do not think will happen), they have changed the way the automobile industry operates forever. That is an example of impact.The first rule of investing is you start by considering the profile of your investors. It’s Investing 101. You don’t ask a 60-year old to invest their savings in Bitcoin even if you stumble upon the technology in 2010.

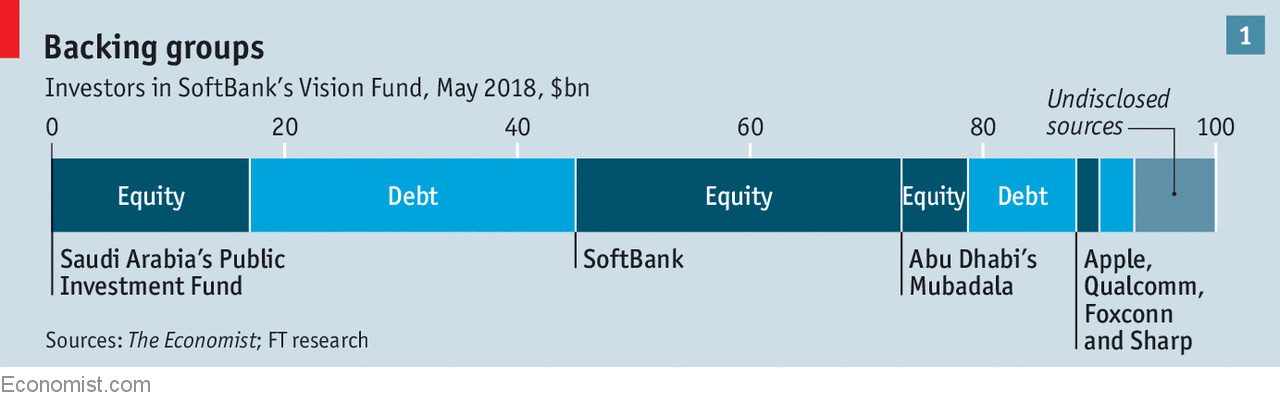

So, let’s consider profile of the investors in our fund.

Let’s start with the GP. SoftBank Vision fund aka Masayoshi Son. A man already worth >$20B through the single best VC investment of all time. Maybe a one-hit-wonder. But a billionaire nonetheless looking to raise his profile in the West.

What about our main LPs? The governments of Saudi Arabia and Abu Dhabi with relatively young rulers at the helm. Oil-rich gulf monarchies flush with cash and eager to invest in the next hot thing. Remember how Gulf-sheikhs bought properties and hotel chains throughout the United States and Europe in the 1980s and 1990s? Well, the sheikhs are back. But what do they see here? The cool kids don’t really wanna own penthouses in NYC and London now. Tech is where all the cool kids are at. And the sheikhs want in. Enter Masayoshi Son - a man with a bold vision who will help them realize this goal. Thus the formation of a fund to invest in all and everything tech. Throw in $50B from the LPs. And look, $50B is no rounding error.

But let’s also not get carried away for this what it might mean to the fortunes of these countries. This is not game-changing money for either of the two main LPs. Abu Dhabi Investment Authority (ADIA), the primary sovereign wealth fund of UAE, owns $900B in assets. And 20-year average returns at this gargantuan fund were just 5.4%. Mubadala, the other main SWF of UAE has another $50-100B. Saudi Arabia’s primary fund is smaller; it has ~$350B of assets. But that’s by design rather than circumstance. For crying out loud, Saudi Arabia opened a new university in the middle of the desert a decade ago. That alone got an endowment of $23B from the government. So yeah, $50B - nothing to smirk at, but let’s not pee our pants either. What would you rather see? $450M spent on a Da Vinci painting? This is just how the nouveaux riche roll. Don’t like it? Well f*ck you as Ben Affleck’s character in Boiler Room would say.

So yeah, maybe our investors don’t care as much as your ordinary LPs about making money. Maybe what you really have is three men (MBS, MBZ and MS) looking to announce their arrival on the world stage. They want to own the most iconic assets of the era. Uber: the most iconic startup of the last decade. Check. WeWork: a real estate company that also does technology? Sign me up, junior. And somewhat unsurprisingly, Saudi Arabia’s PIF notoriously tried to buy out Tesla for $420 in 2018. And maybe our investors don’t mind overpaying and ending up with a 8-10% IRR a decade later. I mean ADIA is only doing 5-6%? How hard can this game be. As long as we all get to own the most iconic companies of the era, we cool bro. Illiquidity discount? We have liquid gold in the ground and we can drill it for <$4 a barrel. Plus, they don’t really have elections so they really mean it when they say that they have a 20/30 year time horizon. Take your time, you can pay them back the money an year or two later. Just make sure you DM them.

Here is a overview of SoftBank’s portfolio companies as of Sept 2019.

Sure, you might notice a few duds (I see you, Fair) But, think of the most iconic companies (ARM, Flexport, Doordash, Oyo, WeWork, Uber, Grab, OpenDoor, Paytm) of the past few years and most of them are here. And look, this portfolio isn’t meant to rival Sequoia’s investment track record. SVF isn’t looking to create some multi-decade investment institution here. They just want to own the most popular companies. Maybe you think B2B SaaS is a great vertical. And hey, maybe you’re right. But that’s not what floats the boat of these investors. They won’t get excited about your enterprise SaaS company that helps hospitals and HMOs. Or helps monitor servers. So f*ck you too Datadog, SoftBank doesn’t want you.

And let’s not lose our sh*t here. SVF is doing exactly what it’s supposed to do. It is an institution deploying capital in private startups at a rate not previously seen. Along the way, it is generating tonnes of headlines and warping the rules of the game. Along the way, their investors are also getting part ownership of the most prized assets. And here is the bet I believe Son and his LPs are willing to make: even if they pay overpay 5x or 10x for a unicorn; if they get to own the next Microsoft, Google or Amazon - holding that company over a 15-year period will more than compensate for all the misses along the way. And on a long-enough timeline, the real net IRR is bound to hit >10%. Along the way, Son and his pals also get a seat at the prized table.

What about ordinary folks like you and me? What’s the bull case for all of us.

Well, for a start, it massively expands the Overton Window. All the stuff we want to say about Silicon Valley and VC that we couldn’t previously say in public, we cheerfully say now and attach SVF to it. Alex Danco has a great post on a Girardian interpretation of how we all processed the WeWork/SVF debacle. I couldn’t possibly do it justice in a couple of lines. Therefore, I include an image here as a teaser to encourage you all to read the full post:

Secondly, we have all been recipients of massive subsidies to enjoy some truly great products (Uber, DoorDash, WeWork). I am reminded of this tweet from a few months back:

So, yay to consumer surplus. Surely, all these subsidies won’t last into the coming decade.

Finally, SVF likely did accelerate the pace of innovation. In as much as it allowed more people to go into startups and more money to be spent trying to build new products, it is likely a good thing for the overall pace of innovation. Most large corporates (with the exception of Amazon) today are cash cows that largely return most cash to shareholders. While this makes financial sense, it isn’t exciting if you are someone hoping that corporate America will lead the charge on innovation. Here is how Peter Thiel grilled Eric Schmidt on this point a few years back:

Lastly, consider this fact: Out of the $481 billion in free cash flow Apple produced over the last decade, it returned 81% to shareholders. Buybacks: $299B; Dividends: $89B

There is a lot of money today earning sub-zero yields, sitting as cash and treasuries or chasing ETFs. Compared to the trillions invested in such ‘non-innovations’, SVF’s $100B remains a pittance. However, in as much as this figure represents an attempt to shake things up, it should be considered a success and be lauded.