So what do these two entities have in common? The obvious answer is the government of Saudi Arabia. Saudi Arabia is the majority LP in Vision Fund, owning roughly half of the $100B fund. And the Saudi government also owns ~99% of Saudi Aramco. I write this piece on the eve of Aramco’s IPO for a neat $1.8 Trillion valuation.

Before we proceed further, let’s start with considering Aramco. The company has tortured investors with rumors of its ‘on-again/off-again’ IPO for two years now. The eventual offering earlier today was a bit of a dud as to how it was structured. Let’s look at how institutional shares (2/3rds of the total offering) were allocated:

So, a direct listing with the majority of proceeds going to Saudi government, Saudi companies and GCC institutional investors. The final allocation to non-Saudis was at best 15%. And let’s remember that the IPO was only for 1.5% of the company’s to begin with.

So, 15% of 1.5% = 0.225% So, after two years of fuss and headlines, foreigners now get to own a quarter of a percentage point of the most valuable company in the world. Let’s quickly get valuation out of the way. Aramco is rumored to have a 2018 EBITDA of ~$224B - valuing it at even 10x (a very modest multiple) that figure easily places the company’s value north of $2T. Taken another way, even if I take future growth as zero and just treat the EBITDA like a perpetuity, discounting it at 10% (way greater than the company’s actual cost of capital), we still end up with a valuation of $2.24T. So, no issues there. If anything, the company seems to be trading at a discount. Of course, the fact that a significant portion of this EBITDA gets paid to the Saudi government (the main shareholder) is likely the reason here as it obscures the true FCF available to ‘shareholders’.

Anyways, valuation isn’t the point of my piece. Although, ironically enough valuation is the only reason the IPO was done. The crown prince wanted to flex his muscles and have the largest public company in the world be Saudi. So, getting a high valuation has always been the main goal. This was clouded under a broader rationale of economic diversification and how this money would benefit the Saudi economy move away from non-oil investments. But that was McKinsey-speak. Let’s be frank and open here - the company raised ~$25B via its IPO and less than $4B of the final sum came directly from foreigners. $4B is small enough that Aramco could reduce capex a bit in 2020 and ‘save that much’ without anyone noticing. Or just issue a small bond and offer 3% yield instead of selling shares. So, call me cynical but the diversification argument fails the smell test.

What is more interesting is that the final allocation makes it now an exercise in money transfer from one arm of the government to the other. If Saudis and Saudi institutions are ultimately the majority participants in the IPO, isn’t it the same money just changing hands? Maybe, maybe. Now let’s turn to the SoftBank Vision Fund. Vision Fund has by now mastered the art of putting money from one pocket to another. Such antics are not unique to government-owned entities and large conglomerates. But it’s the first that I know of for a major VC fund. The Vision Fund playbook for the past few years has been basically this:

Invest in a mildly interesting startup at a high valuation 🚀

Do 1-2 follow-on rounds of financing at even higher valuations. Often, SoftBank is the only investor in these follow-on rounds 🦄

Book accounting gains and show great IRRs/paper profits to LPs 🤓

Earn a nice little management fee while raising Vision Fund II 🤑

Obviously, I’m being overly cynical here. But what I’ve said isn’t entirely untrue. What’s crucial to understand is that Vision Fund can do bullet 3 because it’s an investment vehicle. It is actually mandated by law to do it. Mark-to-market accounting rules require it to carry up the value of its assets at the end of each reporting period. And since, a lot of its own private investments are indeed ‘increasing’ in price over follow-on rounds, the fund has been able to show paper profits.

Let’s use an analogy to explain what is really happening. Let’s say I buy an iPhone for $1000. Next month, I tell my mom that I think my used iPhone is really an asset which is appreciating in value. As such, it is worth $2000. My mom out of love for me tells me that she believes me and lends me an extra $250 based on my new found wealth. I quickly go ahead and decide to invest this $250 in buying a fancy case and Airpods for my iPhone. I then announce to my mom that my phone has appreciated in wealth to $2000. She tells me that she is really happy for me but has no more persona money to lend. Now, until I manage to find a person who is willing to buy this phone from me, this $2000 is just an imaginary figure in my head. And that is how a lot of Vision Fund investments are today in the absence of an actual liquidity event. So, here is how SoftBank’s reported the performance of Vision Fund a few months back in August:

So, a cheery looking graph that I remember was being used to ‘silence’ critics of the fund. The key thing to note however is that it isn’t immediately clear how much of that $20B gain had is realized vs. unrealized. (Maybe it is mentioned somewhere in the footnotes but I’m too lazy to dig) . Anyways, if you’re a n̶a̶i̶v̶e̶ ̶i̶n̶v̶e̶s̶t̶o̶r̶ glass-half-full-guy, you’d be forgiven for thinking that Vision Fund was doing great. I heard an institutional LP argue as much at a recent conference back in late October. But with this week’s announcement of Vision Bank selling its Wag stake for a hefty discount, it is worth considering whether these accounting rules make any sense. More so, should they even be legal/permissible for investment vehicles that invest primarily in illiquid stock of early-stage companies. The only thing that makes a startup interesting (financially speaking) is the ultimate promise of a big payday. In the absence of one, price is an abstract number that gets thrown around among friends. In the early stages, the number is based on a few cute slides and a vision for the future. Ultimately, when the company does become successful - investors generally realize their gains through a sale or an IPO 7-8 years down the line. Most VC firms typically own 10-20% of a company at this stage. But Softbank changed the rules of this game. It would start by investing early at a bold valuation. And then would often do even bolder follow-on rounds at even higher valuations. In the case of WeWork, this was taken to one extreme where it was the sole investor in the $47B round. But SoftBank had already invested twice before in WeWork at that point. As a result of this aggressive capital deployment, SoftBank is reportedly underwater on its more sane investments like Uber.

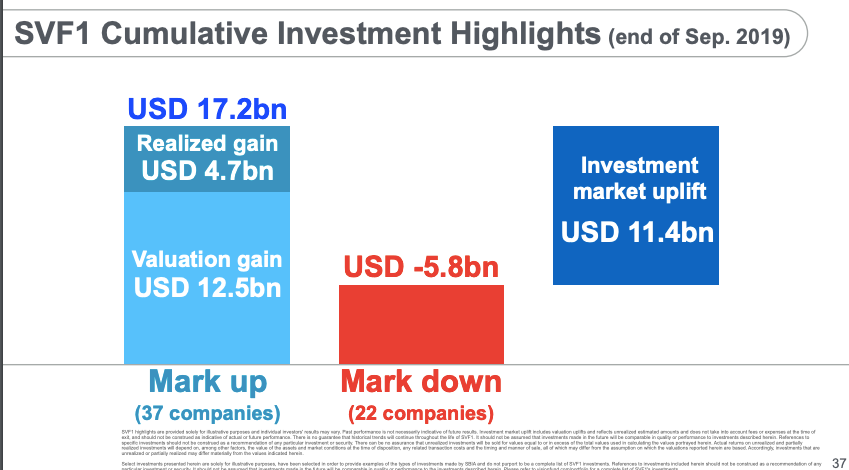

Anyways, here is a slide from SoftBank’s latest investor update delivered last month after all the bad press/WeWork IPO cancellation. This slide is more revealing:

So a more somber looking graph and I suspect there is more pain ahead. And not just for SoftBank. A lot of the current portfolio gains that many private investors are sitting on (including pension funds who are often big LPs in such funds) likely exist in name only. Warren Buffet famously said that is only when the tide goes out do you realize who has been swimming naked. The next recession could expose a lot of people’s bare bottoms.

Scott Galloway famously said, “..if you tell a thirty-something dude he’s Jesus Christ, he’s inclined to believe you”. I think a similar dynamic applies here. If you tell a thirty-something founder that his company is worth a billion bucks, he’s inclined to believe you. What’s also likely is for him to take your money and mess up his cap table. All this while subconsciously knowing that there is no sane way to deliver the growth expected to justify the valuation. So, we can’t expect the founders to be the voices of reason here. Rather, it is the VC funds and regulatory bodies that need to lead on pushing for this change of rules. I read a rumor (on VC twitter) that Sequoia invested in Robinhood at a $7B+ valuation largely because of the presence of SoftBank as the great benefactor of SV. The rumor went something like this: Sequoia didn’t believe the valuation was justified given Robinhood’s relatively modest revenues. However, the presence of SoftBank shifted the calculus. The Sequoia team felt comfortable that a large player (aka SoftBank) or a PE firm would step in and invest in at an even higher valuation in a successive round. If there is truth to this rumor, this is unfortunate and illustrates the true damage that is being done to the tech ecosystem here.

Ultimately, this post isn’t about blame. Our institutions are a microcosm of broader societal shifts. There is a broader shift in society towards an economic reality where intangibles (e.g. brand, data) are the most important part of any company’s success. Consider this graph for companies in the United States and the relevance of accounting measures in valuing companies.

So, the real problem is that accounting/book values have generally become quite meaningless. Mark-to-market is a good faith attempt fix that. It has some benefits. But in the case of institutional investors and private valuations, it only causes harm.

Aramco will definitely be fine. $25B is pocket change for them. The company indirectly owns the world’s largest hydrocarbon reserves. And has access to the GDP of a young population of $35M+ people. Vision Fund faces are more bleak future. Value investors like Buffet/Munger have been huge critics of mark-to-market and the volatility it creates in results. I definitely think a rethink is needed here. Not only does it cause volatility to quarterly results, it completely misaligns incentives between investment funds and startup founders. And ultimately, the follow-on effect from this could cause something similar in impact to the dot-com crash.

To receive more posts like these, sign up for the newsletter: