What Ryanair can teach the insurance industry

Why being the low-cost player is an under-appreciated asset

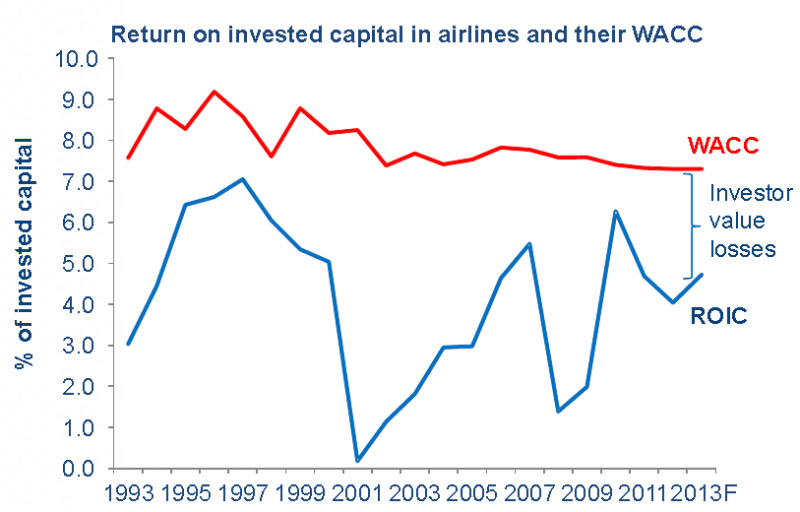

There are few industries as brutal as civil aviation. Even in the best of years, most airlines end up without a profit. As a whole, it has lost investors over the past five decades. Here is a (slightly outdated) graph illustrating just that:

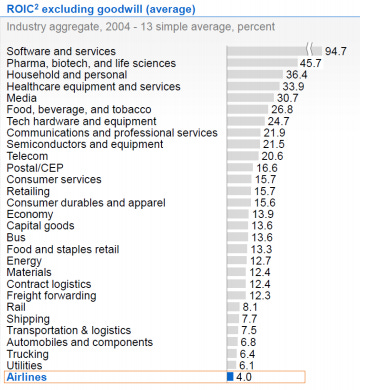

High CAPEX, high OPEX and cyclical demand mean that the industry generally ranks dead last on most measures of shareholder return. For instance:

However, one company in this industry stands out at an exception. Ryanair. Ah yes, the low-cost European budget airline. The company that we all love to hate. The airline that all Europeans have sworn at some point in their life to never take. The company that is so cheap that it once introduced a rule banning employees from charging phones to save on electricity costs. A company so frugal that this quote from its CEO sums up its thinking perfectly:

“One thing we have looked at is maybe putting a coin slot on the toilet door, so that people might actually have to spend a pound to spend a penny in the future. Pay-per-pee. If someone wanted to pay £5 to go to the toilet, I'd carry them myself. I would wipe their bums for a fiver." - Michael O Leary

Anyways, many such juicy nuggets exist about Ryanair’s corporate practices. But I’m only here to discuss Ryanair in the sense that it is one of the few players in a very punishing industry that actually returns a profit. Consistently. Despite having some of the lowest average fares even within the budget segment.

So what’s the secret sauce? Well, the unfortunate one-line answer is: good, old-fashioned expense management. The company’s executives have such a dedication to cost cutting and frugality that it is now ingrained in the company culture. They have combined this with a clever unbundling of the core product (i.e. the privilege to fly) from a host of ancillary products that customers buy quite often. Fittingly enough, even ‘reserving a seat’ is actually an ancillary now with Ryanair. Anyways, there are a lot of good primers written on Ryanair and I encourage you to read them if your curiosity is piqued.

Now, let’s visit an old friend, Michael Porter. Of the five forces fame. Here’s what he thinks are the competitive strategies any company can adopt. There are only three strategies really:

Focus

Differentiation

Cost leadership

These are often summarized in a triangle or 4x4 box like the one below:

I routinely hear of startups that believe focus or differentiation will be their competitive strength. For instance, a company will say that they will focus only on millennials or people with one arm or three legs and so on. Similarly, it is common to see pitch decks talking about differentiation. Lines like ‘We aim to offer a superior customer experience through our app and offer an unparalleled and seamless digital experience’. You know, the usual platitudes. This is all stuff that will make a VC drool if he believes you’re credible as an entrepreneurs.

What is surprising to me is how few startups or incumbent focus on the third competitive strategy as they look to innovate. You don’t see slide decks saying ‘We plan to be the cheapest bas*ards in the land’. Sure, this might be some 10-year vision for a few companies where the use of technology will lead to a better cost structure. But ‘aiming to be a cost leader’ is rarely the starting point. It would be refreshing to see companies aiming for a customer experience so minimal and bare-bones that it meets the bare standards of what is expected. But the catch is it has to be twice as cheap as the next best alternative.

Now let’s talk about insurance. Here is what Warren Buffet said in a letter to a National Indemnity officer with regards to GEICO in 1976.

“I have always been attracted to the low cost operator in any business and, when you can find a combination of i) an extremely large business, (ii) a more or less homogenous product, and (iii) a very large gap in operating costs between the low cost operator and all of the other companies in the industry, you have a really attractive investment situation. That situation prevailed twenty five years ago when I first became interested in the company, and it still prevails.”

Remember this is over decades ago so GEICO is a super small player then. Reading the full letter, I’m surprised as to how few people appreciate that being the low cost operator is probably the single-most important factor in many industries. It is particularly true in insurance where the product is ‘more or less homogenous’. Industry leaders like GEICO understand this and run at sub-20 percent expense ratios. GEICO I believe has an expense ratio of around 15%.

So how does a small startup with large upfront fixed costs compete against the dynamic described above? I believe the answer lies in not differentiating or focus but actually competing on costs. It would be interesting to see a company come and say we actually think a lot of this fancy fluff insurers do (apart from regulatory stuff) is necessary. You want to talk to an agent to buy the policy? You gotta pay extra. You want to talk to an agent when starting the claim? That’s an extra ancillary. And by the way, these agents will likely be in a developing country so you might have to work with an accent to explain yourself. So it might take you a bit longer on the phone. You want windscreen cover? That’s an ancillary too. And so on. That is strip the core product of every possible feature but the bare minimum to meet the regulatory standards. Sure, people will hate this product. They will whine about it to their friends. The NPS for this company will be close to zero or even possibly negative. Just like Ryanair. And yet, the headline price will be attractive enough that people will just keep buying. Many of these are people who buy insurance just to get the legal requirement out of the way. Over time, as the company builds up a policy base and starts to collect premiums, it can spread those high costs and re-invest the money into even cheaper prices for competition.

If the above idea sounds familiar that is for good reason. That is in essence the crux of Clayton Christensen’s idea of disruptive innovation. Many of these innovations typically start with the lowest end of the market. The low-premium, disloyal customers that big players likely won’t be too fussed about. But rather than targeting them with a fancy technology stack or a compelling niche story, you just target them via good old-fashioned low prices. But to achieve those you have to have a compellingly low cost-base. And you have to take every unnecessary feature out of the product. You won’t be hiring engineers in Silicon Valley or London for this. Your website will likely be a simple Wordpress website connected to a payment backend and be maintained by a handful of remote developers. Over time, you might introduce some features. But everything about the product and the business will be simple and focused on achieving and maintaining low costs.

It is common to see companies refer to themselves as the Amazon/Uber/Netflix of industry x. We will be the ‘Amazon of insurance’ is a phrase that I have personally heard at least a hundred times. But what would be really refreshing to hear is someone say the following:

We will be the Ryanair of insurance