“The best minds of my generation are thinking about how to make people click ads. That sucks.” - Jeff Hammerbacher Back in college, I remember an ad that used to follow me online everywhere. I came across this ad recently and was hit by a fond nostalgia for my undergraduate days. Here is the ad:

The ad itself has now been the center of some controversy given that the girls in question are not actually the founders. Today, I want to discuss Everquote, the company that sits behind these ads.

The company was the subject of a fairly critical report by Bonitas research. Now negative analyst reports are hardly anything new. But this particular report did get me thinking about Everquote. And it sent me down a rabbit-hole into the depths of the ad-tech supply chain as I researched the company.

Before we proceed any further, it is important that you read these two articles:

John and Ranjan do a brilliant job of exposing the world of Taboola-Outbrain and the different participants involved in this ad-tech supply chain. However, blaming these two (now merged) companies for everything wrong with online advertising is somewhat unfair. So let’s kick the can a bit further down the road. Let’s look to our friends at Everquote and see how they contribute to this mess.

So, what exactly is Everquote? Here’s what the company’s IPO prospectus had to say:

“EverQuote makes insurance shopping easy, efficient and personal, saving consumers and insurance providers time and money. We operate the largest online marketplace for insurance shopping in the United States. Our goal is to reshape insurance shopping for consumers and improve the way insurance providers attract and connect with customers as insurance shopping continues to shift online..” As is often the case with prospectus statements, the above is obviously pure hogwash. The company neither makes shopping easy, nor does it save anyone time or money. All it does is aggregate leads through a bunch of click-baitey ads and sells these to anyone with a pulse and a credit card. The company thus is one of the enabling forces behind the largest robo-call network of insurance agents. Insurance companies are often panned for having bad customer service. But even in an industry with such a reputation, Everquote outdoes itself on how poor its reviews tend to be.

So, how has the company grown for so long. Let’s start with how the company is unique. Traditional price comparison was simple. You bought a fancy domain, you aggregated a bunch of traffic via PPC and SEO and further sold these leads to insurance/banking companies. The benefits of this model were really in the scale benefits of one player buying all the marketing leads and selling them via a trusted a pay-per-sale model. The success of price comparison in markets like United Kingdom, Italy and Spain was a testament to the benefits of this model.

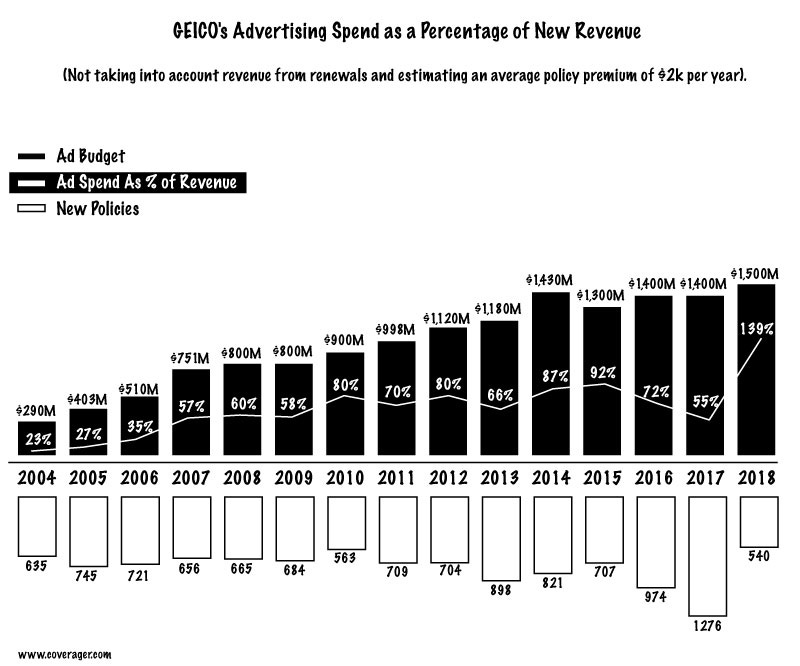

But the United States insurance market has always a different beast. Just for car insurance alone, we are talking about $240B of annual premiums. As a result, it was almost impossible for newer ‘tech’ companies to merely outspend traditional direct players like GEICO, State Farm and Progressive on traditional marketing. Consider this graphic from Coverager around how GEICO’s marketing budget is as a percentage of its New Business Premium. It should give you a good picture of how difficult market entry really is for a new player:

So, GEICO which has 13-14% market share alone spends $1.5B on advertising alone. Against such a backdrop, new players can hardly be expected to make any inroads via traditional advertising channels.

Enter Everquote, a company founded in 2012 looking to ‘disrupt’ car insurance. The company was previously called AdHarmonics and had no such qualms about what it was then. It merely called itself a lead-gen at that point. Now, here are some of the ads that Everquote has A/B tested over the years:

(For further history, see this brilliant twitter thread that helped me learn a lot about the company’s ‘changing’ faces over the years)

What is important to understand is that the above ads aren’t merely traditional pay-per-click ads. They most often appear at the bottom of a news article on ‘respectable’ websites like CNN/Washington Post/Fox(?):

So, what’s the secret potion behind these magical ‘native’ ads? Why, of course it’s our old friends at Taboola/Outbrain that sit behind them. And folks who click on the Everquote ad get redirected to a seemingly genuine news article praising the brilliance of the company and its founding team. Click any further and they get directed to a web form that promises a great car insurance deal in return for a few pieces of information.

Ultimately, when the details are taken, the customer is often left at the landing page of an insurance journey on a website like Progressive or Esurance. And it is only after that the real nightmare for the customer begins. Tonnes and tonnes of calls from insurance agents.

So, what’s going on here?

It seems that early on Everquote realized that it couldn’t beat players like GEICO and AllState at the traditional media or PPC game. So it decided to play dirty. And play dirty it did. It went to the deepest, darkest corners of the web and palled up with folks at Outbrain and Taboola. The partnership was so successful that Outbrain even has a case study dedicated to Everquote on their website.

So, if that’s so easy - why didn’t others in the market follow suit?

Well, two reasons primarily:

Single domain vs. Multi-domain

Most companies operate within the realm of owning one or two domains for their website. As such, the company website is often the most valuable piece of digital real estate any company owns. Thus, while most marketing folks understand that they can drive up traffic to their website by linking to a Kim Kardashian article, this is not a strategy most businesses opt for.

Everquote owns over a 1000 live domains under its name. This ‘multi-domain’ strategy means that it operates under no such limitations. Most of the domains are super-long trustworthy word-mashes like trustyourcoverage.com or receivedoptimizedrates.com. If you go to the actual websites, they generally offer the same everquote.com interface with merely a different ‘name’ slapped on top. If you dig deep into the T&C’s, you notice that the owner is Everquote. But all these pages basically serve as ‘lead forms’ for the Taboola/Outbrain sponsored campaigns. Additionally, these websites also provide some backlinks which help with SEO by improving the mothership’s domain authority. The multi-domain strategy might also offer Everquote some benefits around cross-bidding on PPC.

Cost-per-sale (traditional price comparison) vs Revenue-per-lead (lead-gen)

Everquote shunned the traditional pay-per-sale model of price comparison in favor of a more conventional pay-per-lead model. Despite the high-sounding rhetoric in the company’s IPO prospectus, the company remains very much in the business of selling leads. Here is how agents/insurers can buy these leads via the Everquote platform: (Source: Coverager)

So, instead of offering a one-stop bind solution to customers, Everquote is merely selling leads en-masse to anyone willing to cough up $5 or more (prices are likely higher now). This likely leads to a race to the bottom. With Everquote getting the most price-sensitive consumers who fail to get an online price but only get a series of phone calls in return. This also means that the company is unlikely to get a lot of repeat customers. Over a 5-year horizon, it is unlikely to have even a lot of repeat B2B partners. Progressive, one of their largest customers, decreasing their account-size with them might offer some indications that the current model is under strain.

The lead-gen model might work for a truly ‘push’ non-mandatory insurance product like life insurance. Such products largely involve an agent speaking with someone and convincing them on the phone. Thus, these leads being passed around via such a funnel journey makes more sense. Assurance’s blockbuster sale to Prudential is proof that such a model might work.

However, in the boring world of car insurance shopping, Everquote represents an unfortunate return to the 1990s - the era of banner ads. And while this chum might help bring in some s̶h̶a̶r̶k̶s̶ customers today, such a business won’t last for too long. Indeed, this whole transaction leaves such a putrid smell, that everyone involved is just left wishing that they had never come here in the first place.